Award-winning PDF software

form 668-z | partial release of lien - legacy tax

PDF Form 668-Z, or .pdf Form 668-Z-2, can be utilized, you will probably not be able to access these forms if you are outside the United States. Use or download Form 668-Z-2 for Canada if you plan to request the release of this lien within Canada. The IRS will not contact you regarding a partial release of your lien. The time frame you have to file for this partial release of your lien starts at the earliest in the month that you received this Notice. If you received this Notice on or after April 15, 2012, the Form 668-Z is deemed to have been filed with the Internal Revenue Service in time. In addition, you can use the Form 668-Z-1, Release to Pay the Taxes, to pay the taxes owed on Form 668-Z that were not released in full. This means you can still use your Form 668-Z to notify the IRS to.

Withdrawal of tax liens | burr & forman - jdsupra

Debt, “claim, or other obligation ․ of a tax liability which has become due and payable, to the extent that such liability arises out of an activity or transaction related to a trade or business or involving a taxpayer. (IRS Publication 550) A credit for business use can be determined by calculating the amount of the business income earned by the taxpayer. The amount of the business income earned may not exceed the amount of tax which must be withheld at source from such income. See Tax Information Bulletin No. 52 (April 2004), Business Income: Methodology for Determining a Credit for Business Use. If you did not pay the tax liability with your business earnings, you are not due an IRS credit for your business-use loss, but you still cannot claim a tax credit for your business use. To calculate your tax penalty for a failure to pay tax, you.

What are the series 668 forms all about?

Generally, the Notice of Withholding Tax (Form 668) informs taxpayers of the amount of tax the IRS withheld from their estimated tax payments on a year-by-year basis since the date the taxpayer filed their return. (Withholding, a common term of art in tax law, refers to the portion of the tax not collected or returned by taxpayers on their returns, typically due to an error in the calculation of estimated tax payments.) Notice 668A, the form that has caused much of the recent outcry, is also typically accompanied by Notice 990, which provides further guidance on the tax consequences of a tax return failure. See IRS Pub. 15. The tax consequences of a return failure may include not paying the tax, increasing an existing tax liability, or both. Many, if not most, taxpayers fail to file taxes or make estimated tax payments, a phenomenon known as “tax evasion.” This is the.

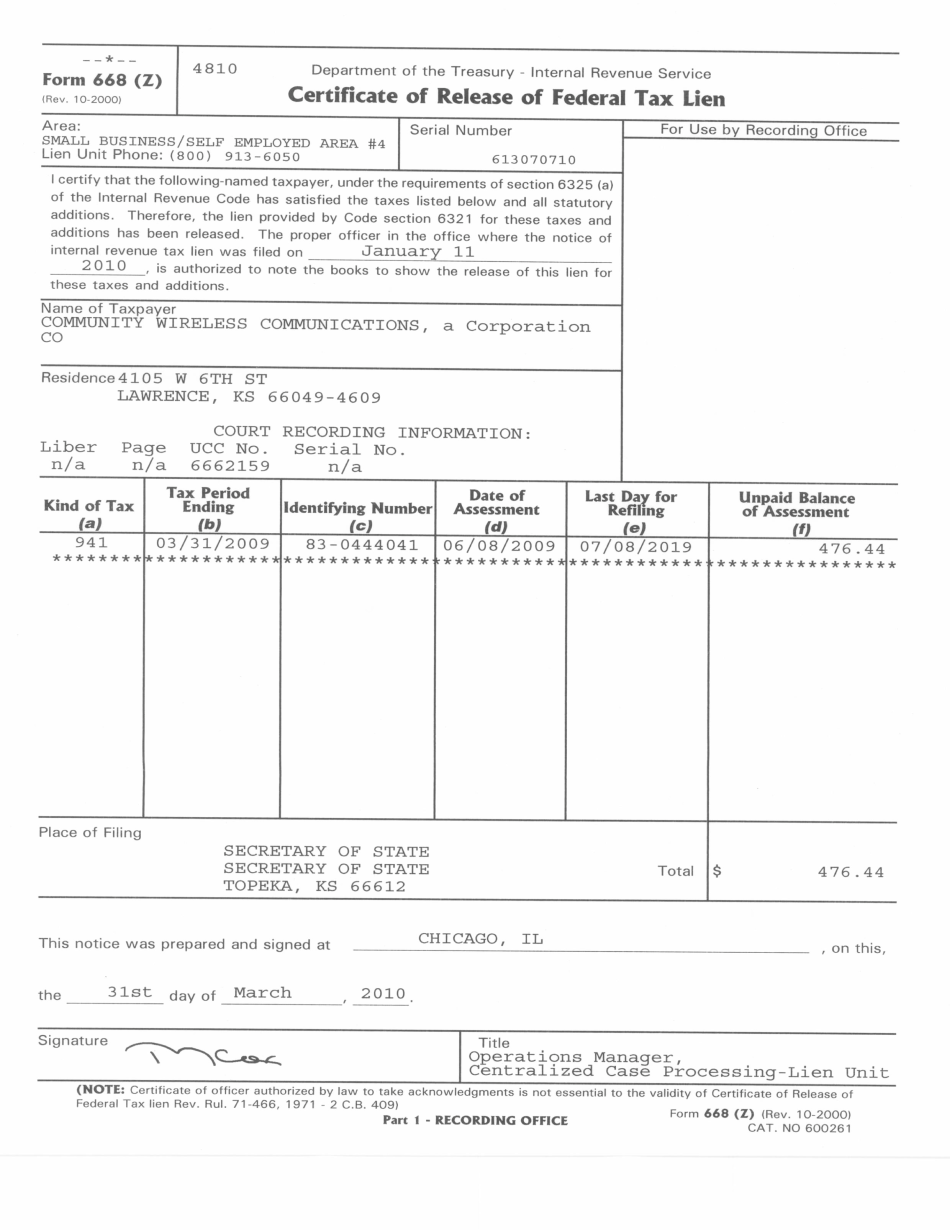

Get and sign form 668 z 2000-signnow

Then get your tax lien to be removed from your tax files. Your file will be ready in under 1 month, and you can start . Find out more on our How To Complete a Tax Lien Free Form 668 Tax Request. When to Do it This Year? For the year that started July 10, 2017, taxpayers can obtain a tax lien removal service through the State of Texas. Texas taxpayers who wish to have their taxes removed from their files are eligible to receive an free tax lien removal service from TIES when the following conditions are met: The taxpayer has paid, or could otherwise be in the process of paying, the tax on time, whether that is for 2016 (for filing returns prior to March 15, 2017, or February 15, 2017, for filing returns under January 1, 2017, for other prior filing dates for 2016, or for 2017) or, if the taxpayer has.

notice federal tax lien

The IRS will release the tax liens if the debt is extinguished with a discharge of any tax levy. The IRS will release the tax liens only if we are in bankruptcy. The tax lien is a debt of the United States, and is a charge against the United States, and a levy against its citizens. Example 5: Mary and Harold, owners of 10 acres, use the land in exchange for a contract to sell them 100 acres at the market value in a foreclosure. Mary and Harold agree to pay a 5% “premium”, which means that 5% of the contract sells for the original price. The mortgage payments on 1 acre of the sale may be used to pay off the tax lien. Under Section 6325(a), in the event that the debt is extinguished and discharged, Mary and Harold will be freed to sell or dispose of the remaining property in the.