Award-winning PDF software

Form 668(Z) Houston Texas: What You Should Know

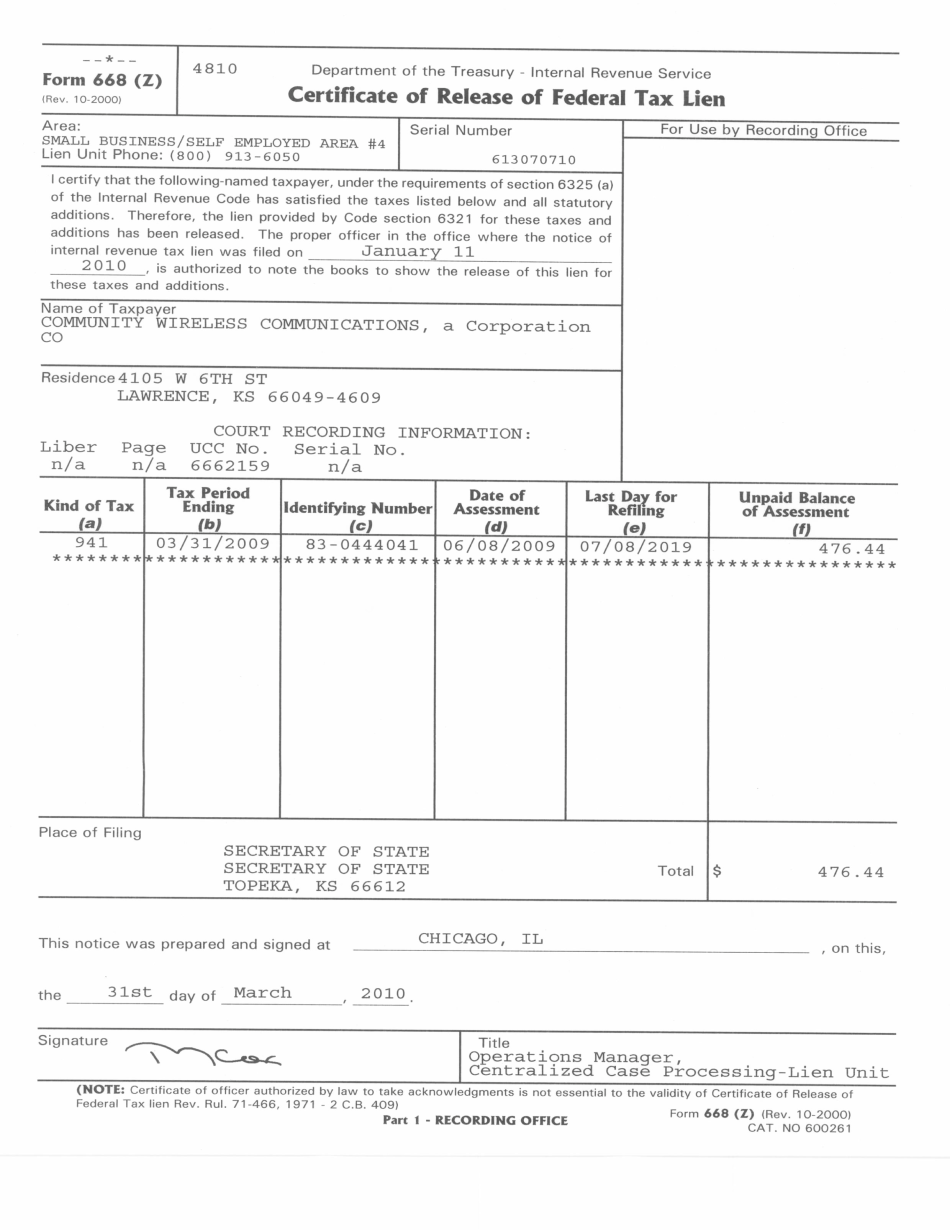

IRS Lien Release Procedures for Taxpayers With Bank Accounts and/or Insurance Contracts — General Lien Procedures The rules governing the release and release of lien documents and interests depend on the status, category and category of the lien document, and the taxpayer's relationship to the IRS. For example, a taxpayer that has no relationship to the IRS will have very little opportunity to negotiate a release. For taxpayers that do not meet the “special case” exception described by IRC Section 7212(c), a release is generally automatic even though there may be some negotiation. Once the release is effected and the IRS has completed examination, the IRS can begin collection actions to collect the unpaid tax due on the balance. For taxpayers that owe income taxes, a release must be approved by the IRS and signed by a representative of the Commissioner of Internal Revenue prior to the notice of a release being mailed to the taxpayer. Categories that do not require a release include: tax lien on property, tax lien on business, tax lien on income, tax lien of any kind, tax lien on any other income (i.e., wages, interest or dividends), and other exemptions. The IRS does not routinely provide information on whether the release will require the consent of a third party if the tax is not paid within three years of the estimated payment date. Taxpayers that choose to accept a release from a third party that is not required to sign a release could be subject to adverse action, including audit, arrest, garnishment and/or criminal prosecution, for failure to make the required third party consent for release. If a tax lien, which is not subject to a release, is not paid within five years of the estimated due date, it can be sold, and any proceeds received should be refunded or offset against the tax that remains unpaid. The IRS does not generally require the release of a lien with respect to noncorporate taxpayers (i.e., individuals, partnerships, S corporations, and other tax-qualified partnerships, trusts, and estates).

Online methods assist you to arrange your doc management and supercharge the productiveness within your workflow. Go along with the short guideline to be able to complete Form 668(Z) Houston Texas, keep away from glitches and furnish it inside a timely method:

How to complete a Form 668(Z) Houston Texas?

- On the web site along with the sort, click Commence Now and go to your editor.

- Use the clues to complete the suitable fields.

- Include your personal info and contact data.

- Make certainly that you simply enter right knowledge and numbers in ideal fields.

- Carefully verify the articles from the type in addition as grammar and spelling.

- Refer to aid portion for those who have any queries or tackle our Assistance team.

- Put an digital signature on your Form 668(Z) Houston Texas aided by the enable of Indicator Instrument.

- Once the form is completed, push Finished.

- Distribute the all set variety by means of e-mail or fax, print it out or help save on the product.

PDF editor allows you to make adjustments with your Form 668(Z) Houston Texas from any world-wide-web connected equipment, personalize it in line with your requirements, indication it electronically and distribute in several methods.